By Kushal Sarawgi on The Capital

Sector Overview-Understanding Indian Savings

India has been a country with one of the highest Gross Savings Rate (GSR) worldwide for a very long time and has peaked its GSR at 37.8% in the year 2008–2009. Soon after which the trends started shifting, and the GSR steadily decline over the past decade. As of the fiscal year 2019, the country touched its 15-year low GSR of 30.1%. On the other hand, it must also be noticed the per capita income of the country has been rising over the past decades and is making new highs every year.

On analysing both these factors together, we can conclude that an average of India has been earning the highest ever, but is saving the lowest (at least in the past 15 years). This also makes sense citing the boost the entire lending ecosystem of the country has seen over the past few years.

Coming back to the article — Although India continues to have a decently high savings rate, the per capita income continues to remain low, when compared with its global peers. Which is worrisome for the current working population as they might be the ones who end up in the boundaries of significant chaos when the situation of urgent money requirement shows-up. Urgency could be in the form of — bearing the hospital treatment expenses of your loved ones, purchasing your dream house which has recently been vacated by its previous owners, or maybe just because you found a perfect holiday package for the upcoming weekend.

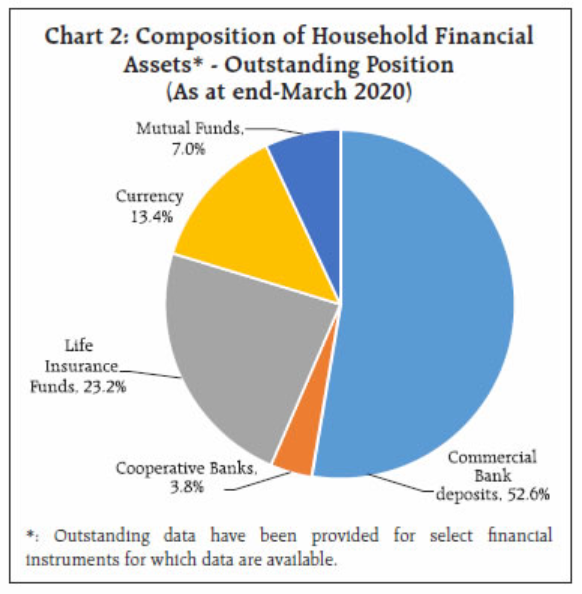

If we take a deeper dive in the assets held by a regular Indian Household we will usually find the following breakdown —

Talking about the numbers — there are a total of 44 Mutual Fund Companies who provide over 2500 mutual fund schemes to invest in, 24 Life Insurance Providers, 34 Non-Life Insurance Providers, over 100 co-operative banks (all varieties incl), and 87 commercial banks (Domestic and International incl) available to park the surplus money earned by an average India.

The Current Saviors

To provide financial guidance in India, one needs to be registered with the financial regulator as a Mutual Fund Distributor (MFD) or a Registered Investment Advisor (RIA). As of date, India has only a little over 2.3 lakh registered Mutual Fund Distributors (a significant proportion are employees of banks), 1305 Registered Investment Advisors, and 1829 registered CFPCM. To put that in perspective, there are over 12.08 lakh LIC agents in the country, leave aside agents from other insurance providers. These guys collectively make up for the entire population responsible for serving the world’s largest demography of 130cr.

On the other hand, there surely is a rise of startups such as Groww, Kuvera, Paytm Money, ETMoney among others who have been helping smoothened the investing experience for investors. However, given the regulatory concerns of India, these apps can at best claim themselves to be as quasi-Robo wealth advisory services. One app which I’ve come across and which stands out of the other regular apps is IndWealth. The company runs on a digital-first business model, wherein the client can transact on their own but can get in touch with experts (not the sales team) when guidance is required with regard to managing their money.

On the traditional side front, keeping aside banking institutions, only an extremely handful sum of institutions have been able to scale their business pan-India while maintaining quality service and client-centricity. One example being Bajaj Capital, a company which started in 1964, with a simple dream of Mr. KK Bajaj and now advises over 41lakh investors on managing their money, which crosses INR27000cr.

A lot of players have also risen in the B2B WealthTech space helping intermediaries service their clients better. The same was being much anticipated as the B2B space continues to remain paper and compliance heavy for intermediaries.

The Future Value

Retirement Expenses is usually one of the largest shares of expense made by an individual, and a simple set of calculations will let you know that you’d need a corpus as big as INR2.7cr just to sustain your lifestyle, considering your monthly expenses to be constant at INR 50,000 per month with a 7% inflation for 20 years. (Which also has an implicit assumption of never spending beyond the limits of INR 50,000)

On the other hand, research by The National Skill Development Corporation tells us that ~90% of the country’s population above 15 years of age earn less than INR 88,000 making it difficult for people with limited income to sustain their family, leave aside saving and building on wealth.

2020 was supposed to be the year when India would have matured to start fetching its demographic dividend, but in case the benefits of this dividend are not cultivated and nurtured in the proper manner the payoffs would be much higher, whenever the time comes. Hence, it is important that the WealthTech space emerges soon, and enables people across the globe to embed within themselves small habits of savings for a better future.

https://twitter.com/thecapital_io

WealthTech: Finding The New Glitter was originally published in The Capital on Medium, where people are continuing the conversation by highlighting and responding to this story.

from The Capital - Medium https://ift.tt/3gJInQn

0 Comments