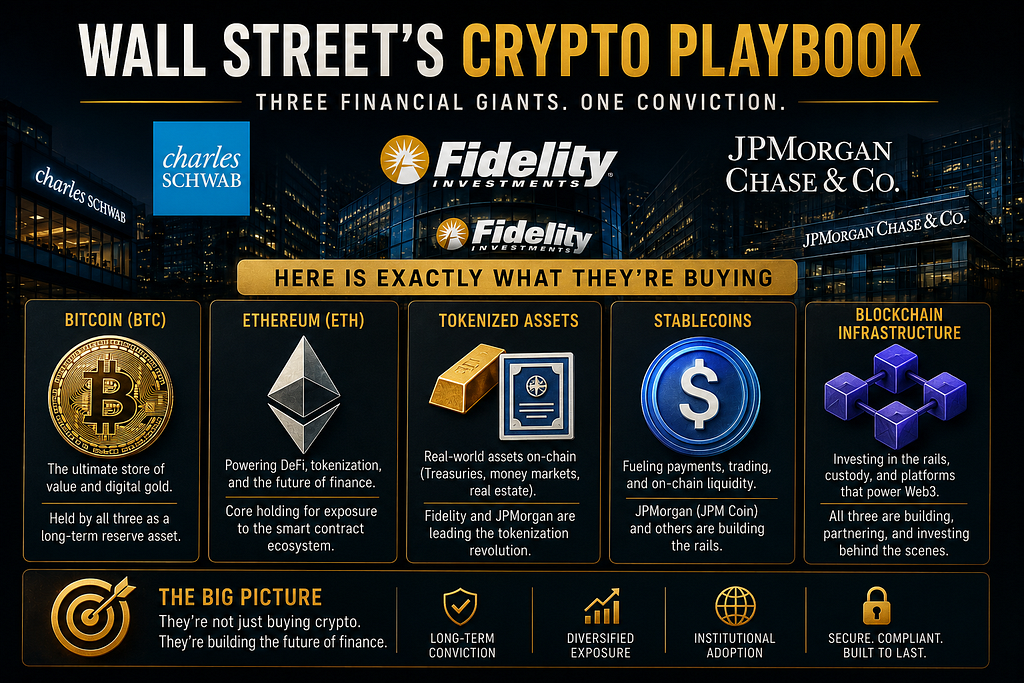

Charles Schwab, Fidelity, and JPMorgan Are All In on Crypto Now. Here Is Exactly What They’re Buying

When the three biggest names in American finance all make the same bet in the same 12-month window, it stops being a coincidence and starts being a signal.

For years, the official Wall Street line on cryptocurrency went something like this: volatile, unregulated, speculative — maybe a curiosity for retail traders, but certainly not a place for serious institutional money. Jamie Dimon famously called Bitcoin a “fraud” in 2017. Fidelity was the quiet outlier, building infrastructure in the background while its peers scoffed. Charles Schwab kept crypto at arm’s length, offering futures exposure while staying carefully clear of actual digital assets.

That era is over.

In a compressed and dramatic stretch spanning late 2025 into mid-2026, Charles Schwab, Fidelity, and JPMorgan Chase have each made moves that would have seemed unthinkable just three years ago. This isn’t about dabbling. This is about three institutions that collectively manage trillions of dollars in client assets deciding that crypto is no longer a category they can afford to sit out. The question worth asking — the one most retail investors are not asking loudly enough — is: what, specifically, are they buying? And what does it mean that they’re all moving at once?

The Regulatory Unlock That Made All of This Possible

Before getting into what each institution is doing, you need to understand why they’re doing it now. Because the timing isn’t accidental.

A series of regulatory shifts quietly dismantled the legal barriers that had kept major banks and brokerages on the sidelines. In March 2025, the FDIC rescinded its prior-approval requirement for banks engaging in permissible crypto activities — a policy that had functioned as an effective veto on bank-level crypto participation. Two months later, in May 2025, the OCC issued guidance clarifying that national banks could buy and sell customer-custodied crypto assets and outsource execution with proper risk management. By February 2026, Fidelity had obtained OCC approval for bank-based crypto custody and execution outright.

The SEC followed in April 2026 with an interim statement clarifying broker-dealer registration for certain crypto interfaces. And underpinning all of it was the passage of the GENIUS Act, which created a federal framework for stablecoin legislation for the first time. Combined, these changes didn’t just reduce uncertainty — they handed the biggest institutions in finance a legal roadmap to build on.

Wall Street had been watching and waiting. Once the runway was cleared, they didn’t walk. They sprinted.

Charles Schwab: Spot Bitcoin and Ethereum, Starting Now

Schwab’s move is the one most retail investors should pay attention to, because it directly changes what 35 million brokerage clients can do inside an account they already have.

In May 2026, Charles Schwab began rolling out spot cryptocurrency trading, starting with Bitcoin and Ethereum. This is not crypto futures, not an ETF, not an indirect exposure vehicle — this is direct ownership of the underlying digital assets, available through the same interface Schwab clients already use to buy Apple stock or Treasury bonds.

The strategic logic behind the launch is not complicated, but it is significant. Schwab already estimates that its clients hold approximately 20% of the US spot crypto exchange-traded product market — meaning roughly one in five dollars invested in Bitcoin and Ethereum ETFs already sits inside a Schwab account. Those clients have been going elsewhere to hold the actual coins. Schwab, in effect, has been watching a revenue stream walk out the door, and it has now decided to stop letting that happen.

Schwab has been explicit that Bitcoin and Ethereum are just the beginning. The firm has indicated plans to expand beyond those two assets and add transfer capability over time, meaning clients will eventually be able to move crypto between Schwab and external wallets. Internally, Schwab has also been exploring the development of a stablecoin — a move that would position it to play in blockchain-based settlement and liquidity, not just as a trading venue but as a financial infrastructure provider.

For context on the demand it is walking into: visits to Schwab’s crypto platform surged 90% year-over-year heading into the launch. The pent-up interest was never the question. The regulatory and operational infrastructure just needed to catch up.

Fidelity: The Veteran Playing Its Deepest Cards

Fidelity has been the most crypto-forward of the major traditional brokerages for years. It launched the Fidelity Wise Origin Bitcoin Fund (FBTC) in 2024, which now holds $13.4 billion in assets under management. It has run Fidelity Digital Assets, a dedicated institutional crypto custody and trading operation, since 2018. It sponsored an Ethereum ETF alongside its Bitcoin fund. It is not a newcomer to this space.

What changed in 2026 is the regulatory standing of those operations. With OCC approval secured in February 2026 for bank-based crypto custody and execution, Fidelity can now operate its digital asset infrastructure under the same regulatory umbrella as its conventional banking activities. That matters because it changes who can access those services — specifically, it opens doors with institutional clients like pension funds and endowments that have strict counterparty and regulatory requirements.

Fidelity’s positioning in the institutional market is particularly aggressive. Its Digital Assets research team has published guidance recommending that long-term investors target 0–5% crypto exposure in a portfolio, with the explicit argument that even a 2% allocation to Bitcoin improves annual retirement spending capacity by 1–4% while increasing loss risk by less than a percentage point. For an asset management firm of Fidelity’s scale, that kind of research publication is not neutral commentary — it is a client education strategy designed to move allocation behavior.

Fidelity currently holds more Bitcoin under management through its ETF products than nearly any other firm except BlackRock. As of late 2025, Fidelity’s FBTC was the consistent second-place issuer in the US spot Bitcoin ETF market by inflow volume, often pulling in hundreds of millions of dollars in single-day inflows. The competitive moat it has built in digital asset custody and ETF infrastructure over eight years of early investment is now paying off in a market that has decisively gone institutional.

JPMorgan: The Blockchain Play No One Is Talking About Loudly Enough

JPMorgan’s crypto strategy is more complex than Schwab’s or Fidelity’s — and arguably more consequential. While the bank’s CEO has remained publicly skeptical of decentralized cryptocurrency as an asset class, JPMorgan’s operational moves tell a very different story.

The bank’s Kinexys platform (formerly known for JPM Coin) has been processing institutional payments on a private blockchain since 2020. As of 2026, that platform processes over $1 billion in daily transactions, primarily in corporate treasury operations and cross-border payment settlements. Its Onyx division has expanded into tokenized collateral networks, programmable payments for corporate clients, and repo transaction platforms.

But the most significant development came in 2026, when JPMorgan launched a tokenized deposit token on Base — Coinbase’s public Layer 2 network built on Ethereum. This is a significant public signal from a bank that had previously confined its blockchain operations to private, permissioned networks. Moving onto a public blockchain indicates that JPMorgan now views interoperability with the broader crypto ecosystem as an asset rather than a risk.

In December 2025, JPMorgan also began exploring institutional spot crypto trading — a riskless principal model that allows the bank to facilitate trades without holding crypto inventory on its own balance sheet, reducing counterparty risk while capturing trading fee revenue. This mirrors the same direction Schwab has taken with its own custody and execution model.

And then there is the tokenized deposit network. In June 2026, JPMorgan, Citi, Bank of America, and other major US banks announced plans to build a shared tokenized deposit network, operated by The Clearing House, targeting a launch by mid-2027. The explicit strategic purpose: to compete with stablecoins. If customers begin holding dollars in stablecoin form at scale, banks face deposit flight. The tokenized deposit network is designed to give blockchain-native payment capabilities — 24/7 settlement, instant transfer, programmable money — while keeping deposits within the regulated banking system.

For JPMorgan, crypto is not a product category. It is an infrastructure war.

What $59 Billion in ETF Inflows Actually Tells You

Zoom out from the individual firm strategies and a broader pattern comes into focus. US spot Bitcoin ETFs have now accumulated over $59 billion in cumulative net inflows since their January 2024 approval. In May 2026 alone, Bitcoin ETFs registered over $1.6 billion in monthly inflows, even amid market volatility. BlackRock’s IBIT holds over $66 billion in assets. Fidelity’s FBTC holds over $13 billion. Ethereum ETFs have attracted hundreds of millions in institutional inflows alongside them.

The composition of that capital is not retail money chasing headlines. It is pension plans, family offices, endowments, and institutional allocators making structured, long-term portfolio decisions through regulated vehicles. According to research from the institutional sector, 68% of institutional investors now either hold or plan to invest in Bitcoin ETFs. That number would have been unrecognizable four years ago.

The institutional thesis for Bitcoin and Ethereum is now standardized enough to be put in a prospectus. The assets have liquidity. They have custody solutions from qualified custodians. They have price discovery through regulated markets. They have allocation frameworks published by Fidelity, VanEck, and others. The remaining friction for most allocators is largely reputational and operational — and firms like Schwab removing the operational friction is precisely what accelerates the reputational shift.

What This Means If You’re a Retail Investor

The entry of Schwab, Fidelity, and JPMorgan into direct crypto services changes the calculus for retail investors in several ways that are easy to underestimate.

First, it changes access. Millions of investors who held back from crypto because they did not want to open a Coinbase account, manage a software wallet, or navigate an unfamiliar interface can now access Bitcoin and Ethereum through the same brokerage they have used for decades. Friction is a genuine barrier, and Schwab just removed it for 35 million people.

Second, it changes perception. When institutions of this size and reputation make structured bets on digital assets, it moves the Overton window for what counts as a legitimate investment. Crypto in your Fidelity retirement account looks different from crypto on a speculative exchange — not because the asset changed, but because the context did.

Third — and this is the point most commentators miss — it changes liquidity. Every major financial institution that adds crypto custody and trading infrastructure increases the depth and stability of those markets. It reduces the dominance of crypto-native exchanges in price formation. It creates more institutional counterparties and more mechanisms for large capital to move in and out efficiently.

None of this eliminates Bitcoin’s volatility, Ethereum’s execution risks, or the genuine uncertainty around where crypto fits long-term in a diversified portfolio. These are not endorsements; they are observations about the structural direction of the market.

The Bottom Line

Schwab is buying Bitcoin and Ethereum — and bringing 35 million clients along for the ride. Fidelity is buying Bitcoin, Ethereum, and regulatory infrastructure that lets it custody those assets inside the regulated banking system. JPMorgan is buying the rails: blockchain payment infrastructure, tokenized deposits, and a stake in the future architecture of how money moves.

Three different strategies. Three different positions on the risk-reward spectrum. One shared conclusion: the financial system is integrating crypto, not as a fringe asset class, but as a permanent component of modern market infrastructure.

The question is no longer whether Wall Street is in on crypto. They are, demonstrably, irrevocably, and with billions of dollars of committed capital and infrastructure investment behind them.

The question now is whether the rest of us were paying attention while it happened.

This article is for informational purposes only and does not constitute financial or investment advice. Cryptocurrency investments carry significant risk. Always conduct your own research before making any investment decisions.

Schwab, Fidelity & JPMorgan Go All-In on Crypto in 2026 was originally published in The Capital on Medium, where people are continuing the conversation by highlighting and responding to this story.

from The Capital - Medium https://ift.tt/OaXekJj

0 Comments